Insurance policies are often filled with terms that can be difficult to understand, particularly for the average insurance buyer. Of these terms, “named perils” and “open perils” are some of the easiest to confuse.

When it comes to understanding what their coverage entails and ensuring their policies are adequate enough to protect against the most common risks, homeowners need to have a basic understanding of how perils are used in their insurance contracts. What is a Peril? In insurance, the source of a particular loss or damage is considered a peril. In that regard, a peril can be any number of hazards or events that lead to a claim. Often, insurance contracts use the term peril to describe what risks are covered under a particular policy. Common perils in home insurance policies can include, but are not limited to, the following:

It should be noted that not all perils are covered in a given policy. For instance, while an earthquake is considered a peril by definition, it may be excluded from a residential insurance policy. Homeowners would need dedicated earthquake insurance in this instance. This is an important distinction when it comes to understanding your insurance and what is or isn’t covered. That’s where named and open perils come into play. Named and Open Peril Policies: Which One is Right for You? There are effectively two types of homeowner policies to be aware of to ensure you are appropriately covered: 1) Named peril insurance policies—Under these types of policies, coverage kicks in only following losses from perils or damages specifically named in the policy itself. This often includes things like fire, theft, falling objects and vandalism. Essentially, if the policy doesn’t specify whether or not a given peril is covered, it likely isn’t. Under these types of policies, the burden of proving that a named peril caused a loss lies on the insured. 2) Open peril insurance policies—Open peril policies (sometimes 1.referred to as all-risk or all-peril policies) provide coverage for all perils except those specifically excluded in the policy itself. While often more expensive than named peril policies, open peril policies are more comprehensive and usually have higher limits. In addition, under these policies, the burden is on the insurance company to prove whether a peril is excluded. Exclusions may vary by policy but generally apply to perils that require standalone insurance or are altogether uninsurable. The type of policy that’s right for you will depend on your specific situation. For instance, those that live in natural disaster-prone regions will need a different kind of policy than those in lower-risk areas. When determining what coverage to elect, it’s a good practice to inventory your property and assess the most common risks to your home. A qualified insurance broker can help you through this process, helping you secure the coverage that makes the most sense for you. To learn more contact TWFG Spring / The Woodlands today.

0 Comments

More than 50 people, mostly children, have been infected by the measles in the United States this year. This particular outbreak concerns southwest Washington and northwest Oregon. Nationwide, though, the Centers for Disease Control and Prevention (CDC) states that eight other states (California, Colorado, Connecticut, Georgia, Illinois, New Jersey, New York and Texas) have reported cases of measles in 2019, bringing the total of reported cases to 79.

What is measles? Measles is a highly contagious illness caused by a virus called rubeola. People are most susceptible to contracting this illness in early childhood. In the current outbreak in Washington and Oregon, the majority of the cases involve children between 1 to 10 years old. Measles usually causes fatigue, runny nose, cough, slight fever, and head and back pains. In later stages, it can cause a high fever, Koplik’s spots (small white dots) inside the mouth and a rash that starts around the hairline and spreads downward. Measles has a 25 percent hospitalization rate, is not treatable and has no cure. The virus can lead to serious complications, such as encephalitis, or inflammation of the brain. In some extremely severe cases, measles and its complications can be fatal. How can the measles be prevented? Measles can be prevented with the measles, mumps and rubella (MMR) vaccine. This vaccine is typically given in two different doses, the first being administered between 12 to 15 months of age and the second being administered between 4 to 6 years of age. The CDC reports that the two doses together are 97 percent effective at preventing the disease, while just getting one dose is 93 percent effective at preventing the disease. Without being vaccinated, you’re at risk of contracting measles, especially because it is a highly contagious illness. If you live in an area that’s experiencing a measles outbreak, call your doctor for recommendations on what to do. Your doctor may recommend staying in your house until the outbreak subsides.  Did You Know?

If your home becomes uninhabitable for reasons covered in your renters insurance policy, the insurance company will reimburse you for your temporary living expenses until you are able to find a new place to live. Renters insurance is there to not only protect the belongings in your home, but so much more. There are so many misconceptions when it comes to what renters insurance is and what it covers. Here are some common myths about renters insurance: I don’t have enough stuff to get renters insurance.

My landlord’s insurance will cover the damages to my belongings.

Personal belongings are the only things covered under renters insurance.

I can’t afford renters insurance.

We spend a lot of time and energy filling our living spaces with items that make it feel like home—it only takes one unexpected event to have it all stripped away. Renters insurance can give you peace of mind knowing that you and all of your belongings are covered. For your quote on Renters Insurance in Spring Texas call TWFG Insurance Spring / The Woodlands 281-466-1310.  Manufactured homes, also commonly referred to as mobile homes, are built in a factory and moved to a chosen location, they aren't much different than a site-built single-family home — but obtaining coverage specific to your mobile home is essential. A standard homeowners insurance policy will not cover your liabilities in the same way this specific policy will.

The Basics A mobile home insurance policy will provide coverage for your home and property such as the following:

Additional Endorsements For added protection, consider purchasing these endorsements:

Top Ways to Save:

Call TWFG Insurance Spring / The Woodlands for your quote on mobile home insurance today 281-466-1310.  The internet, smartphones and other online technologies have helped businesses streamline their supply chains and inventories. However, human error, software incompatibilities between vendors and a lack of transparency can cause even the most efficient operations to experience time-consuming and costly errors.

Online cryptocurrencies like bitcoin depend on a technology called blockchain that can instantly share, secure, verify and store records simultaneously. As a result, many businesses are using blockchain systems to implement efficient and secure recordkeeping systems. What is blockchain and how does it work? Blockchain is a new type of shared, encrypted recordkeeping system that can be seen in real time by everyone involved in a supply chain or other business operation. These systems work by recording a separate record, or “block,” every time a process is updated. Essentially, each block in the system serves as a digital puzzle piece that verifies the next record, creating a digital chain. Each block is encrypted and can’t be changed, since altering any information in the record would be like taking a piece out of a finished puzzle and trying to change its shape. Advantages of blockchain Because each stakeholder in an operation keeps a separate copy of blockchain records, the systems allows for a large amount of transparency and communication. Businesses can also customize how users see information in a blockchain system. For example, an online retailer could let a customer view their orders and shipping statuses, but not their full inventory system. Blockchain technology can give businesses an instant picture of both large and small-scale operations, such as a single product’s location or real-time sales figures. And since records can’t be altered or viewed without permission, they’re extremely safe from cyber attacks and data breaches. Potential applications Here are some of the potential benefits of a blockchain management system:

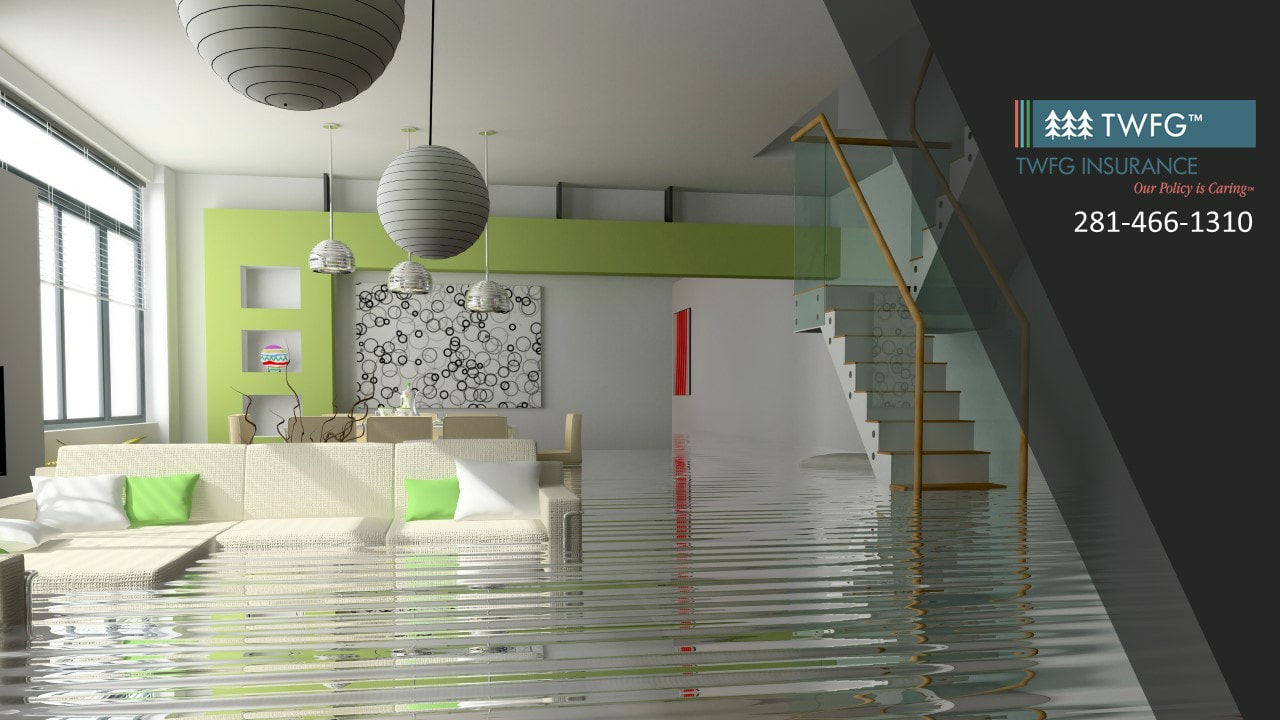

Heavy rain, storm surge, hurricanes and other severe weather events can lead to devastating floods that cause extensive damage. According to the Federal Emergency Management Agency (FEMA), flood damage totaled over $8 billion in 2017 and many of the affected areas are still recovering from the impact.

After a flood hits your business, you’ll still have expenses such as building leases, employee payrolls and cleanup costs. And because any business interruption means that your revenue will be lowered or gone altogether, you’ll need a source of income quickly. Although flood insurance is there to help you recover and rebuild your business, you need to know how to make a claim so that you can get all of the coverage you can as soon as possible. Starting the Claims Process You can start the claims process immediately after a flood. However, before you call us at (281) 466-1310, you should make sure you have the following information:

When the insurer that issued the flood policy gets notice of your loss, you may be able to qualify for an advance payment before the inspection. However, these payments are at the discretion of the insurer and shouldn’t be relied on when you’re planning your recovery process. Pre-inspection Steps After the claims process has started and local officials have determined that it’s safe, you should return to your property to prepare for an inspection to assess the damage. Here are some steps to take before an inspection:

The Inspection Process Once a claims adjuster arrives to inspect your business, make sure to record their contact information. After walking through the National Flood Insurance Program’s claims process, the adjuster will inspect your property and take measurements and pictures of the damage. If an adjuster finds that your business has extensive damage, you may qualify for an accelerated claims process to help you begin repairs immediately. Your adjuster may also have advice for you based on your specific policy. Making Repairs and Other Resources When working with contractors, vendors and third parties after a flood, it’s important to keep copies of all receipts, bank statements, invoices and other documents that show how you paid for repairs. These items may be used as permanent records in case your business floods in the future, and they could affect how much you’re compensated. Getting your insurance coverage after a flood is key, but you have other resources at your disposal. FEMA’s website has a number of resources and programs you can use to recover. You can also contact TWFG Insurance - Spring / The Woodlands for any questions on your flood policy or for resources to help you reduce your damage with pre-incident plans.  A new year brings new issues for HR professionals to contend with. Some challenges are similar to previous years (overtime uncertainty), while others are more unique and complicated (legal marijuana and employment). Despite inherent difficulties, staying tuned in to these six trends can keep you ahead of the game in 2019. Ignoring them will only put you behind.

Below are the top trends to monitor in the coming months. 1. Opioids, Marijuana and the Workplace Opioids have been concerning employers for the last few years, and quietly ravaging the country for even longer. In 2017, the opioid crisis was declared a national emergency due to tens of thousands dying each year from prescription painkillers. Many of these tragedies started with a legal prescription after a common medical procedure. Beyond their deadly risks, opioids also cause absenteeism and performance issues in the workplace. Opioids are difficult to detect in a drug test and even harder to perceive without one. Knowing this, it’s critical to modernize your drug policy to address opioids and offer resources for alternative pain management strategies. Legal marijuana is also complicating drug policies. Similar to opioids, marijuana is increasingly difficult to detect, with the growing popularity of oils and edibles. Moreover, the drug is legal for medical use in 30 states, making testing legally tricky. You may find it easiest to adjust your drug policy to focus on workplace performance. For instance, clearly prohibiting impairment at work or the promotion of drug use through paraphernalia. Adopting a zero-tolerance policy may backfire with state laws, so be sure to have legal counsel review your policy before enforcing it. 2. Leave-related Issues Did you know that 47 percent of employers were very challenged by cross-state leave laws and 43 percent found it extremely difficult administrating leaves in general, according to a recent XpertHR survey? With ever-expanding legislation, it’s not too surprising. Multistate businesses must contend with different state laws, but even smaller employers can find themselves juggling laws between localities. Without proper guidance, handling common requests like family leave, sick time and reasonable accommodation under the Americans with Disabilities Act can be a nightmare. The first thing employers must do is determine which leave laws apply to them, remembering that certain localities might have different rules. Other aspects, like which leaves can be used concurrently and proper leave documentation should come next. And, of course, proper employee communication is a must—not just putting policies in a handbook, but posting leave notices as well. 3. Soaring Health Care Costs Paying over $15,000 annually for each employee’s health care in 2019 sounds like a bad dream, but it’s the real cost trend. With rates surpassing $680 and $20,000 for single and family coverage, respectively, employers are scrambling to cut costs wherever they can. Yet, that can be easier said than done. Some organizations are encouraging workers to utilize telemedicine or virtual care as a way to trim costs. By “visiting” a doctor online for minor health issues, patients can save a trip to the hospital. And, since it’s virtual, everyone saves money. Another cost-saving strategy is the consumer driven health plan (CDHP) model. This strategy empowers employees to control their health care decisions and choose care that best suits them. Since employees use a savings account to help offset costs from their high deductible health plans, they are incentivized to pick more affordable options. 4. Wage and Hour Concerns Hire more workers or pay overtime? That’s the question growing businesses must ask themselves. With overtime changes looming in the first quarter of 2019, you may think it’s easier to hire more workers at lower salaries. But, depending on your situation, that may not be true. Many states are primed to raise their respective minimum wages in 2019. What’s more, the majority of those rates are already higher than the federal minimum. If you’re considering hiring more workers, check to make sure you know how much you’ll have to pay them in your state. The same goes for federal contractors. As for salaried employees, it looks like we won’t know anything about the overtime rule until at least March 2019. This leaves the current overtime threshold at $23,660. Experts expect that number to increase to between $32,000 and $35,000—far lower than the $47,476 rate initially proposed in 2016. This means you should keep watching for regulatory updates in the coming months. 5. New Technologies HR is always looking for new ways to streamline and improve its processes. In 2019, it appears that people analytics and recruiting technologies will be at the forefront of the trend, according to professional HR organization Toolbox. People analytics is a way of tracking things like employee engagement data, training program effectiveness or ad placement success. The practice examines human data and crunches the numbers so you have a better idea of the return on investment. Need to know if your employees feel appreciated? Want to discover which methods employees are using to communicate with each other? This is where people analytics can help.  Maybe you've never heard of umbrella insurance -- it's not advertised much, and unlike car and homeowners insurance, no one requires you to carry it. But it's something everyone should consider, because for a low premium, it gives you a ton of financial protection against bad luck and unreasonable people.

What is Umbrella Insurance? Also called excess liability insurance, this policy works with your auto and homeowners or renters insurance. Essentially, it makes sure you're thoroughly protected financially if you're found responsible for injuring another person and a court decides you should pay the resulting expenses. What does "regular" insurance cover, then? Your primary insurance (that's your auto, homeowners or renters insurance) typically provides some liability coverage and might be enough to pay for all the damages resulting from a minor incident. However, it probably won't be enough to cover the repercussions of a more severe unexpected accident. Who should consider umbrella insurance? Umbrella policies aren't just for wealthy people with lots of assets. Could you afford to lose all the money you've saved, even if it's only a modest sum? And if you don't have any assets to seize, or if your assets aren't valuable enough, umbrella insurance will protect you from having your wages garnished. What does it cover? Umbrella insurance typically covers things like third-party claims for medical care, lost wages, pain and suffering, and attorney's fees. And it doesn't just cover you, the policyholder; it covers everyone in your household. Having a teenage driver is a good reason to have umbrella insurance, for example. Call TWFG Spring / The Woodlands for your quote today 281-466-1310.  Looking at almost two consecutive years of rising costs, the September 2018 IHS Markit PEG Engineering and Construction Cost Index report revealed an index reading of 62.1, up 3.2 points from August.

The survey’s creators expect overall costs to continue to rise over the next six months, reaching a reading of 79.8, the highest it’s been since 2012. Contributing to rising costs is damage from hurricanes Florence and Michael, which are expected to put even more demand on construction services while materials and labor remain limited. Although the work will keep contractors busy, homeowners and businesses will have to be patient during the recovery process. The 25 percent steel tariffs could have a significant impact on construction costs as well. In fact, a Northern Utah wastewater treatment plant saw its price tag increase by $25 million after the tariffs. With steel prices jumping by 31 percent since January, developers may rethink future large-scale projects. FATIGUE: A JOB SITE HAZARD A recent survey by the National Safety Council found that 69 percent of workers feel fatigued at work, exposing themselves to on-the-job accidents and injuries. The workers facing the most risk of fatigue-related accidents are those who do shift work, particularly in industries like construction. In fact, 100 percent of construction workers surveyed reported experiencing at least one fatigue risk factor. The survey also unveiled a disconnect between employers and employees. Ninety percent of employers recognized fatigue as a safety concern, compared to only 72 percent of employees. HELP WORKERS FIGHT FATIGUE It is important for employers in safety-critical industries to make sure their workers understand the risks of fatigue. In order to keep workers safe, encourage them to take the following precautions:

It is also critical to train supervisors to recognize the symptoms of worker fatigue so they can intervene and assign alternate, safer job duties when applicable. |

RSS Feed

RSS Feed